Life Insurance Delay: What to Do When the Payout Is Stalled

Life Insurance Delay: What to Do When the Payout Is Stalled

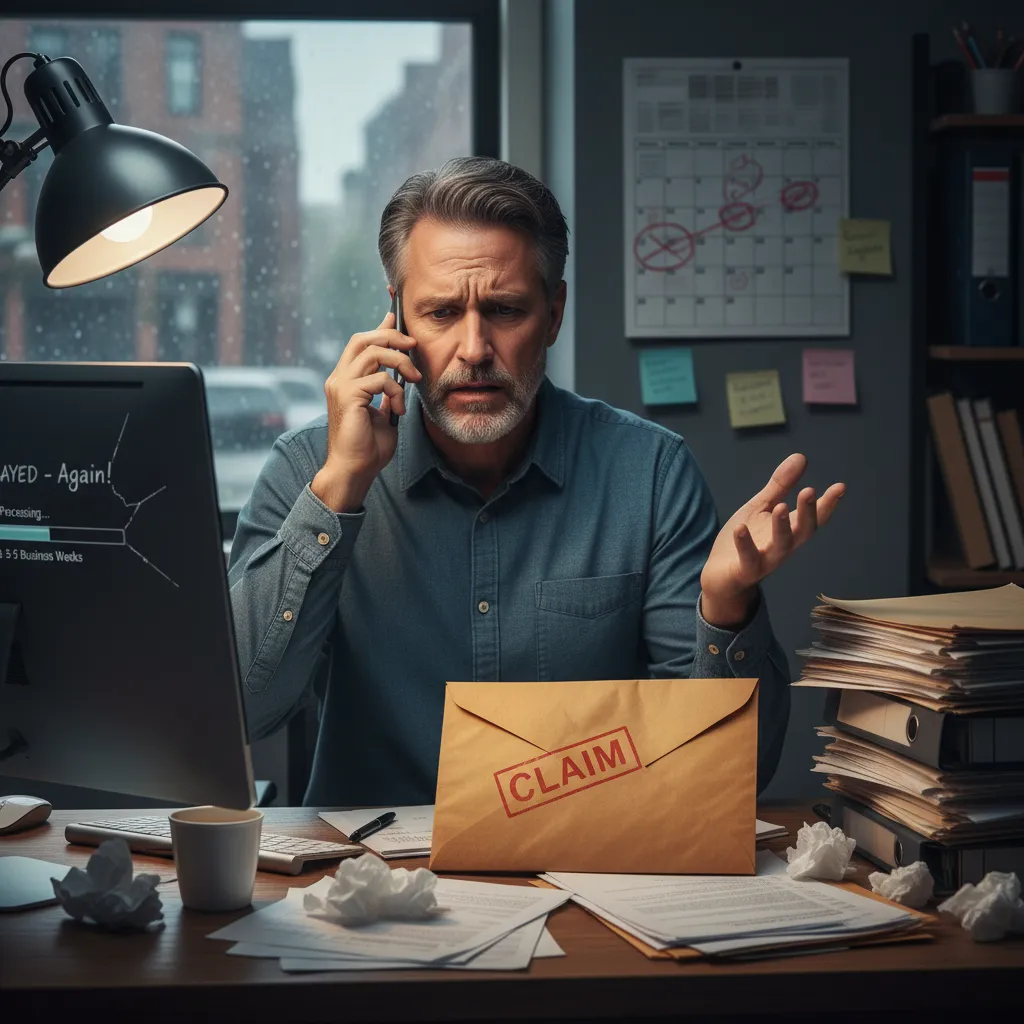

Losing a loved one is hard enough. Dealing with the financial aftermath should be the easy part, especially when there's a life insurance policy in place. You expect the process to be simple: you submit the death certificate, fill out a few forms, and the check arrives in a couple of weeks.

But for many families, that's not what happens. Instead, you get silence. Or worse, you get a "status update" that asks for documents you already sent. Or a notice that the claim is "under investigation."

Weeks turn into months. The funeral bills are due, the mortgage doesn't stop, and you're left wondering why a multi-billion dollar company is sitting on your money. If you're stuck in the "limbo" of a life insurance delay, here is how you move things forward.

Why Do Life Insurance Companies Delay?

Insurance companies are for-profit businesses. Every day they hold onto your money is another day they earn interest on it. While most delays aren't necessarily "malicious," they are often the result of bureaucratic inertia or "red flag" triggers that may not actually apply to your case.

Common reasons for delay include:

- The Two-Year Contestability Period: If the policy was less than two years old when the person died, the company has the legal right to investigate the original application for any misrepresentations.

- Homicide Investigation: If the cause of death was anything other than natural causes, the insurer may wait for a police report to ensure the beneficiary wasn't involved.

- Missing Documentation: Sometimes it's as simple as a missing signature or a certified death certificate that "got lost" in their mailroom.

- Internal Backlogs: Often, the company is just understaffed and your file is sitting at the bottom of a stack on an adjuster's desk.

The Cost of Waiting

A delay isn't just annoying; it's expensive. Most people rely on life insurance to cover immediate costs like funeral services (which average $7,000 to $12,000) or to replace the income of a primary breadwinner. When that money doesn't show up, families often have to dip into savings or use high-interest credit cards just to stay afloat.

Step 1: Audit Your Submission

Before you get aggressive, make sure the ball is actually in their court. Log into your beneficiary portal or call the customer service line and ask for a specific list of every document they have on file.

Check for:

- The Claimant's Statement (completed and signed)

- A certified copy of the Death Certificate

- The original policy (or a lost policy affidavit)

- Any supplemental forms they requested

If they have everything, ask for the name and direct extension of the examiner assigned to your file. If they can't give you one, that's a sign your claim is stuck in a general queue.

Step 2: Know the "Interest" Rule

In many states, insurance companies are required by law to pay interest on life insurance proceeds if they don't pay within a certain timeframe (usually 30 days). When you talk to the company, mention this. Ask them, "Since the claim has exceeded the 30-day window, what is the current accrued interest on this payout?"

Sometimes, just reminding them that the delay is costing them money is enough to get your file moved to the top of the pile.

Step 3: Send a Formal Demand Letter

If you've called three times and you're still getting the runaround, it's time to stop being "nice." A phone call is easily ignored. A formal demand letter is not.

A demand letter serves as a legal notice that you are aware of your rights and are prepared to take further action. It creates a formal record of their delay, which is vital if you eventually have to file a complaint with the State Department of Insurance.

What your demand letter should include:

- The policy number and the name of the deceased.

- The date the claim was originally filed.

- A list of all documents you have provided.

- A specific deadline for a decision (usually 10 to 14 business days).

- A statement that you will contact the State Insurance Commissioner if the claim isn't resolved.

You can write this yourself, but many people find it easier to use a service like howtowritea.com. For $9 to $29, the platform generates a professional demand letter that uses the right terminology to get an adjuster's attention. It's much faster than trying to research the laws yourself and much cheaper than hiring a lawyer, who might take a 33% "contingency fee" just to do exactly what this letter does.

Step 4: Send It via Certified Mail

Never send a demand letter via regular mail. Send it USPS Certified Mail with Return Receipt Requested. This gives you a tracking number and a signature proving the company received it. Once they sign for that letter, the "clock" officially starts. They can no longer claim they didn't know you were waiting.

Step 5: The "Nuclear Option"

If the deadline in your demand letter passes and you still don't have a check, it's time to involve the government. Every state has a Department of Insurance that regulates these companies. You can file a "Consumer Complaint" online.

Include a copy of your demand letter and your certified mail receipt in your complaint. When the Department of Insurance contacts a company, they usually get a response within 48 hours. Insurance companies hate being on the regulator's radar.

Don't Let Them Stall

The money in that policy doesn't belong to the insurance company; it belongs to you. They have had years to collect premiums; they shouldn't take months to pay out.

If you are tired of the "we're still reviewing it" excuse, take control of the process. Use howtowritea.com to draft your demand letter today. It only takes a few minutes, and it's the most effective way to turn a "delay" into a "delivery."

Your family deserves that peace of mind. Go get it.