The Silent Phone: How Elena Broke a 6-Month Life Insurance Delay

The Silent Phone: How Elena Broke a 6-Month Life Insurance Delay

When Elena’s husband, David, passed away after a long battle with heart disease, she was heartbroken but prepared. David had been a meticulous planner. He had a modest $250,000 life insurance policy that he’d paid into for twenty years. He always told Elena, "If anything happens to me, this will pay off the mortgage and keep you in the house."

Elena filed the claim two weeks after the funeral. She sent the death certificate, the original policy documents, and the completed claim forms via priority mail. She expected a check within a month.

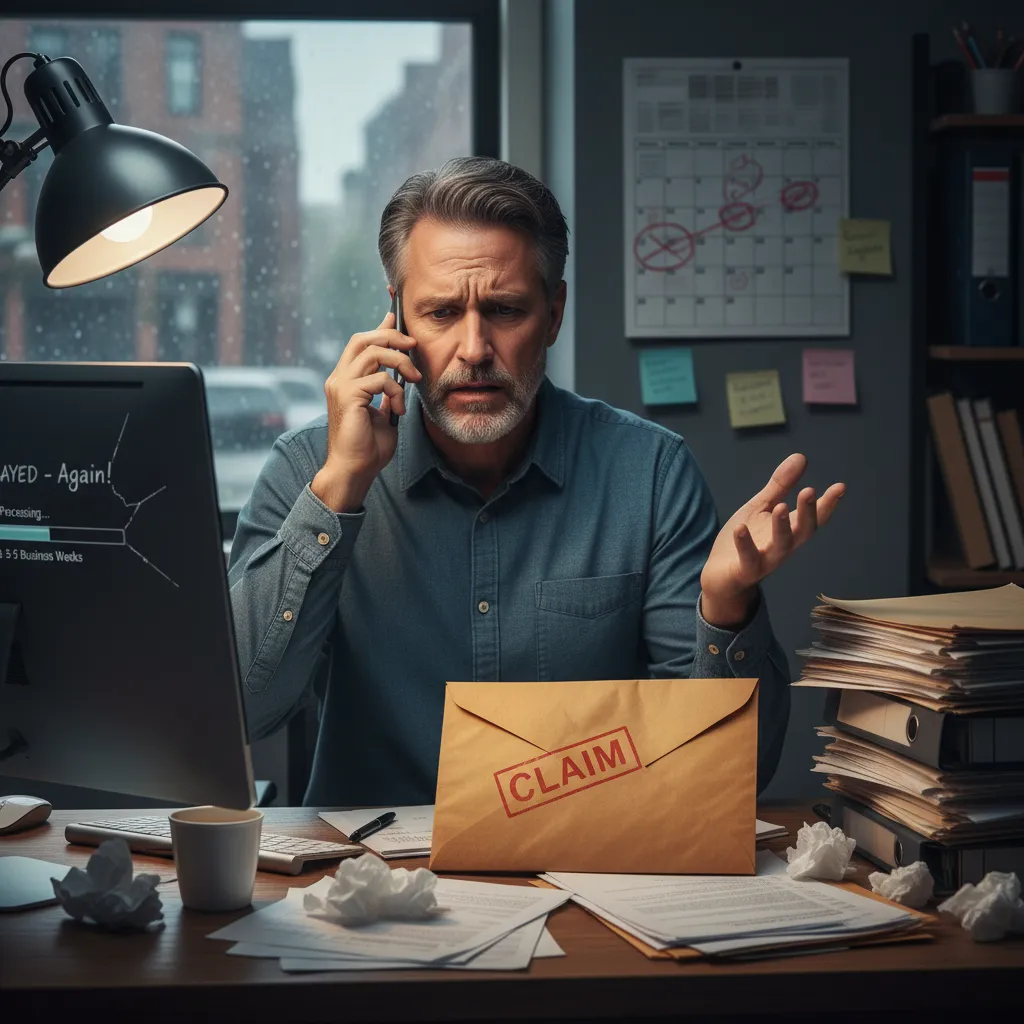

One month turned into two. Two months turned into four.

The "Administrative" Black Hole

Every time Elena called the insurance company, she got the same script from a different customer service representative.

"We're still reviewing the medical records, Mrs. Miller."

"We're waiting on a response from the attending physician."

"The claim is currently with our senior underwriting department for final verification."

Elena was drowning. Between David's final medical bills and the sudden loss of his income, her savings were disappearing. She had already used her credit cards to cover the property taxes. She felt like a pest every time she called, but she was desperate.

By month five, the insurance company stopped giving her updates. They just said, "The claim is pending. We'll contact you if we need anything."

The "Contestability" Trap

Elena eventually learned what was really happening. Because David had increased his coverage slightly eighteen months before he died, the insurance company was using the "contestability period" as an excuse to dig through twenty years of his medical history.

They weren't looking for proof that David had died—they already had that. They were looking for a reason not to pay. They were looking for a single missed doctor's visit or an undisclosed "pre-existing condition" from 2012 that they could use to void the entire policy.

David was a healthy man until his late 50s. There was nothing to find. But by "reviewing," the insurance company got to keep David’s $250,000 in their own investment accounts, earning interest for themselves while Elena struggled to buy groceries.

The Turning Point

At a coffee catch-up, Elena’s friend Sarah mentioned that her brother had gone through something similar with a car insurance claim. "Stop calling them," Sarah advised. "Calling doesn't leave a trail. You need to put it in writing, and you need to make it sound like you're ready to sue."

Elena was intimidated. She couldn't afford a lawyer. Most of the attorneys she called wanted a 33% "contingency fee." Handing over $80,000 of David's legacy just to get the company to do what they promised felt wrong.

That’s when she found howtowritea.com.

The Demand Letter

Elena didn't need a lawyer to argue a complex legal case. She just needed the insurance company to stop stalling.

Using the online generator, she created a formal demand letter. It didn't plead for help. It didn't mention her credit card debt. Instead, it was clinical and firm. It cited the state’s "prompt payment" law, which required insurance companies to pay interest on delayed claims. It pointed out that the 60-day window for a standard review had passed three times over. It set a hard deadline of 10 days for a final decision before Elena would file a formal complaint with the State Department of Insurance.

She spent $29 on the letter and another $8 sending it via USPS Certified Mail with a Return Receipt.

The 72-Hour Miracle

The letter was delivered on a Wednesday. On Friday afternoon, Elena’s phone rang. It wasn't the usual customer service rep. It was a "Senior Claims Adjuster."

"Mrs. Miller, I’m calling to apologize for the delay in your claim. It appears there was a breakdown in communication with our medical records vendor. We have completed our review and have authorized the full payment of $250,000, plus accrued interest."

The check arrived on Tuesday.

Why It Worked

The insurance company wasn't "confused" or "waiting on a vendor." They were playing a numbers game. They stall thousands of claims every year, knowing that a certain percentage of people will just wait quietly or give up.

When Elena’s formal demand letter hit the adjuster's desk, it changed the math. The company realized that Elena:

- Knew her rights regarding interest payments.

- Knew how to escalate the issue to the Department of Insurance.

- Was creating a paper trail that could be used in a "bad faith" lawsuit.

Suddenly, stalling Elena’s claim became more expensive and riskier than just paying it.

If your life insurance claim is stuck in "review," don't be a "polite" voice on the phone. Be a name on a certified letter. Use howtowritea.com to force the company to take you seriously. Like Elena found out, sometimes the most powerful thing you can say is nothing at all—just send the letter.